(Free) Capital Buddha Explorations 1: Micron Technology

Short Overview

The DRAM industry (which represents around 70% of Micron’s revenue) was suicidal. It was about as effective as the airline industry at destroying shareholder capital. Commodity products, fast product cycles, rapid technological obsolescence, capital availability, huge competition, limited pricing power, and technological theft risks to top it all off!

However, I believe that the industry may have hit an inflection point which has gone relatively unnoticed. So much so that a lot of the conditions I named above no longer present a threat to Micron.

Consolidation of Supply, Fragmentation and Secular Growth of Demand

DRAM used to be an easy business to enter. VC capital was widely available to hardware companies. You could raise capital, build a fab, hire a few grad-school engineers, then start competing in the DRAM business by supplying growing PC demand for memory. DRAM technology was in its infancy, so it was relatively easy to shrink nodes on a wafer and build new fabs to provide bit growth.

The main problem was that you’d be selling DRAM to an oligopoly of PC makers who would dictate price. The other problem was that this was a capital-intensive business with cowboy competition and rapid technological change. As a result, industry supply and inventory were never under control. This created deep cyclicality, meaning that DRAM producers got wiped out or acquired in the brutal downturns.

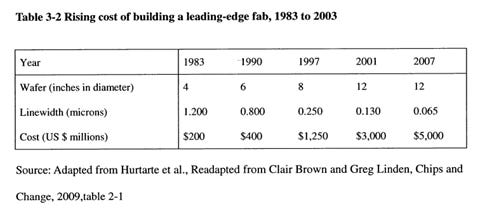

Over time, DRAM became harder to make. It became increasingly difficult to find talent, given the opportunities for engineers in software and other rapidly growing tech fields. VCs and other fresh capital exited the space as the risk-reward got lower. At the leading edge, investments reached the billions (before even a single chip was made!) – and that was only if you could attract engineers, suppliers, and customers to your new venture to compete against the incumbents.

Today we see three surviving firms after brutal cycles: Samsung, SK Hynix and Micron. The three combined companies have 95% share of the DRAM market. The cyclicality of the business has reduced substantially due to the Big Three exercising capital discipline to make sure supply roughly matches demand. Technological gains and node shrinks are also harder to make without flawless execution and billions of capex – which makes the natural restriction of the supply side easier than the past.

However, supply consolidation only tells part of the story. After all, the newspaper industry also consolidated the supply side somewhat – but still didn’t work because advertising and circulation revenues spiraled downwards. Therefore, any synergies on ink savings could not make up for the fact that the product became obsolete relative to the internet.

The DRAM demand story is different to the newspaper demand story. End markets for DRAM have grown double digit over the years and diversified into many different streams. PC, laptop, and networking end markets have been consistently growing. COVID pulled forward laptop demand due to work-from-home trends. The cherry on the cake is that mobile, data center and automobile markets have exploded in the last ten years, providing the DRAM market with ongoing secular runways. The average mobile phone and automobile keeps increasing, leading to ever larger upgrade and replacements cycles in terms of bits shipped. And we are just getting started with buildouts/upgrades of data centers.

Demand Drivers of DRAM

According to Micron’s earnings transcript, DRAM and NAND spend has grown from around 10% of total semiconductor spend to 30% today. Here’s an extract from Micron’s 28th September transcript:

“As a result of growing memory and storage content per device, DRAM and NAND now account for an ever-increasing portion of the bill of materials for our customers. DRAM and NAND TAM share of the semiconductor industry has steadily grown over the last two decades from around 10% to approximately 30% today. The AI and 5G revolution is only in its infancy, and as these secular growth drivers gain further traction, we expect new data-intensive applications to continue to fuel significant increases in DRAM and NAND TAM.”

This trend looks set to continue. The processor chip space, however, is quite competitive. GPUs can be used instead of CPUs for some workloads in data centers. And Google recently came out with a TPU which let them save football fields of data centers had they instead built with GPUs. However, memory seems to be an absolute bottleneck. Just because you decrease the processing needs of a computing task, doesn’t mean that memory needs go down.

In other markets we see a similar story. I haven’t seen an iPhone upgrade with worse image quality, and I haven’t seen storage requirements going lower either. End users always find a way to fill the extra space with content or build applications to max out hardware. On the development side, fewer and fewer developers learn in a hardware-constrained environment, meaning that much new software development today is not extremely efficient. Thus, DRAM and NAND requirements look to increase in coming years across the board. Cloud providers accentuate this trend somewhat, as companies scale up compute by switching to the Cloud without having to invest in capex and talent to maintain internal infrastructure. What this does is let companies throw more ideas at the wall and not worry about their IT scaling – though usage will almost certainly go up.

AI will be a massive step change for memory demand. Here’s an excerpt from NVIDIA’s Q2 transcript call:

“AI model sizes is doubling every 2 months.

It's doubling not every year or 2 years, it's doubling every 2 months. And so you could imagine the size. We're now talking about training AI models that are 100 trillion parameters large. The human brain has 150-plus trillion neurons. And so that gives you a sense of the scale of AI models that people are developing.”

AI requires orders of magnitude increases in dataset size to gain incremental accuracy improvements. Loading up on DRAM and NAND investment is probably still the most cost-efficient way to achieve greater deep-learning accuracy, with huge payoffs for end users. An example of AI’s industrial payoff is a Walmart project to forecast inventory levels. Data scientists, specializing in retail, born in the hardware-constrained world were beaten out by a 20-year-old with zero retail knowledge, who brute-forced an AI model to forecast inventory levels more accurately than retail specialist data scientists. The winning model was data-intensive and cost a lot in terms of processing but saved Walmart millions in inventory. Such stories are likely to appear in greater frequency as AI applications and hardware gets built out. In summary, AI provides massive tailwinds for the DRAM and NAND industry – but will take some time for demand to really pick up.

Management

Sanjay Mehrotra co-founded SanDisk, which specialized in flash memory products. He was CEO at the time of sale to Western Digital – with a price tag of $19 billion in cash and stock. It’s not clear how much stock he owned at the time due to part of his shares sitting in a family trust, but it’s safe to assume that as a founding CEO he didn’t need another job to pay the bills. He could have played golf every day and invested his own money very successfully, given his insight into a rapidly growing and consolidating semiconductor industry.

I have no idea about management structure or motivation in detail. However, my hunch is that he took the job not only to have fun – but maybe that Micron was on the cusp of an inflection point which he had special insights into.

Mehrotra has installed a new management team at Micron, some came with him from SanDisk. The team has taken Micron to a technological lead over Samsung and SK Hynix in many key memory and storage product lines. They have also put in place a great capital allocation framework, buying back 148 million shares at an average price of around $47 over the last 4 years – equivalent of about 10% of today’s market cap. The management team is aided by the overall industry structure, which is now an oligopoly exercising restraint in capacity expansion, leaving Micron with the ability to earn excess cash and return it to shareholders.

Risks

Chinese Competition and Technology Theft

Korea’s industrial conglomerate, Samsung, made a big bet on DRAM in the 1970’s. The technology was licensed to Samsung by none other than Micron, who was running out of cash in an industry downturn. The technology was easier to develop for the reasons I mentioned in the first part of this write-up. However, the other piece was that Korea’s semiconductor program was centralized and very coordinated, given the small size of the country and dire need for economic growth.

There’s this notion that China can compete at the leading edge of the DRAM segment, the same way Korea did. I believe there would be difficulties with China succeeding in the same way as Korea with a similar playbook.

Firstly, the barriers to entry on the leading edge are sky high. Billions must be invested before a single chip is made. This was different when Samsung first started out in Korea. Secondly, suppliers such as ASML are already struggling to build enough machines to keep up with demand. My guess is that they’d think twice before selling machinery to an unknown Chinese DRAM start-up as opposed to their main customers such as TSMC and Samsung. I have no idea whether this was a constraint for Samsung, but I would bet that if Samsung was willing to pay for an EUV machine, they would get it ahead of a Chinese upstart. The third problem is talent shortages. Why would a semiconductor engineer at the leading edge – probably in their mid 40’s – be willing to risk their career and perks, and move their family to China for quick cash? The likelihood is not zero, but I’d still say the opportunity cost is high for such a move. Fourthly, though the Chinese intention is to invest heavily behind a local DRAM industry, the webs of bureaucracy and different competing regulatory factions make it hard to have a coordinated and centralized investment approach like Korea in the 1970s.

Sanjay Mehrotra himself, however, acknowledges that a future Chinese leader in DRAM is inevitable. He also mentions that it is very hard to do – and that throwing cash at DRAM will not necessarily get the desired result. Overall, I believe that the risk of a leading-edge Chinese DRAM competitor in the very near future is muted.

Geopolitical

A lot of leading-edge production (Micron included) happens in Taiwan. There is a semiconductor ecosystem for manufacturing, talent, and knowledge which cannot be quickly replicated elsewhere. China considers Taiwan part of the motherland – and obviously any military occupation or pressure from China towards Taiwan would change the investment analysis of Micron.

In the worst case, the leading edge fabs could be wiped out or rendered useless. Engineers might be flown abroad to safety, meaning that manufacturing stops in the most profitable plants. Or even if manufacturing can continue, property and IP rights over plants may change if there is a transition to more Chinese-based law.

I don’t expect this to happen, as it would benefit no one – including China. I expect pragmatism to prevail – however, I also acknowledge that this is a deep historical conflict where pragmatism might not be the only voice in the room. There is no avoiding this risk as it’s not easy to move the whole semiconductor manufacturing ecosystem. Micron’s leading edge fabs being rendered inoperable would take away significant operating profits and result in asset write-downs which would destroy a lot of upside in the company.

Cyclicality and Irrational pricing

The industry has typically been very cyclical. However, in the last 5 years, due to rationalization of supply in DRAM, the industry has demonstrated supply discipline and remained profitable even through severe industry downturns.

DRAM and NAND sales are dependent upon very complex supply chains and product cycles. For example, if there is a microprocessor component shortage which stops laptops being made then DRAM and NAND sales would be adversely affected. Additionally, if cloud providers such as Amazon and Microsoft have overestimated cloud demand, then they would slow down their ordering of DRAM for the next year to allow them to eat away excess inventory. Micron has experienced all these disruptions and more in the last 3 years and remained profitable the entire time.

The DRAM side of the business looks in very good shape, and should be able to weather the storm, regardless of cyclicality and inventory in end markets. However, the NAND business – which represents around 30% of Micron revenue – is not consolidated enough to make a safe bet on profitability through the cycle. NAND bit demand is increasing by 30% per annum, due to widespread flash storage adoption and increases per device (can you imagine your next iPhone with less storage than your current one?). The suppliers of leading-edge NAND include a Chinese state-owned YMTC which has industry leader ambitions beyond pure profitability. Fiercer competition in NAND leads me to believe that this side of Micron’s business will not run as easily as the DRAM business. However, there are signs of further consolidation, with SK Hynix acquiring Intel’s NAND business for $9 billion in a deal announced in 2020. In addition, Western Digital is offering $20 billion to buy Japanese competitor Kioxia. There’s a good chance that the NAND business eventually becomes consolidated enough to offer supply discipline – but we’re not there yet.

Technology Risks

The greatest risk in my mind is technological risk. If there is better technology than DRAM capable of memory, then an investor would rely on Micron making a strategic pivot to the new technology. There aren’t many (if not any) substitutes available for DRAM – but in high tech industries this can change quickly. For storage, the NAND business overtook HDDs in terms of cost and industrial uptake. And over the past few years, NAND has accelerated faster due to the dropping cost of the technology vs. HDD.

There are no specific technologies which appear to be gaining traction versus DRAM and NAND for memory and storage – but this is the main risk which needs to be monitored throughout the life of the Micron investment.

EUV Transition Risk

The second greatest question mark is the transition from multi-patterning to EUV lithography. Rivals Samsung and SK Hynix have been using the technology for years and have managed to achieve manufacturing scale and knowledge with the process. Micron has famously decided to start the process of experimenting with EUV late, instead choosing to milk multi-patterning technology for a few more years. This decision comes with some risk:

1) Micron must now hire engineers who understand the EUV process and learn how to use this process at scale to achieve yields that let it retain gross margin.

2) EUV machines are in short supply. Priority supply goes to large customers such as TSMC and Samsung. There is no guarantee that Micron can make itself a priority customer in the eyes of ASML (builder of EUV machines).

If the transition is botched, this could endanger Micron’s current technology lead and gross margin profile.

Valuation

Instead of doing an excel sheet, I’ll take a different route. Micron is very profitable, producing $29 billion in earnings in the last 4 years – with $7 billion going towards buybacks at (in my opinion) very good prices, and the remaining FCF going back towards capex. The business fundamentals in both DRAM and NAND are improving every day. There is nothing apart from a ridiculously high offer, geopolitical event or technological paradigm change that would force Micron into a sale – given that the company has ample liquidity and profitability.

Given that Micron repurchases shares every year, and has shown to be repeatedly FCF positive, it’s not crazy to believe that Micron’s earnings multiple can converge towards the S&P 500 market multiple of 28.7 purely from repurchases. Stripping out the cyclicality of earnings by taking the average of the last 4 years, we end up with $7.25 billion X 28.7 to get us to a potential market cap of $210 billion, or around $187/share – 170% upside from the current price. Additionally, given the strong economics of the DRAM business, and the improving economics of the NAND business, I expect further tailwinds to earnings and ultimately re-rating of the business.