No. 22: Amazon Limits to Scale, Game Selection Part 2, Baijiu Reflections

No. 22: Amazon Limits to Scale, Game Selection Part 2, Baijiu Reflections

It’s good for me to revisit physical limits to understand how big companies like Amazon can actually get – before I dangerously extrapolate continued 30% per annum growth. I tried to go through some back-of-the-envelope numbers for Amazon’s US E-commerce business.

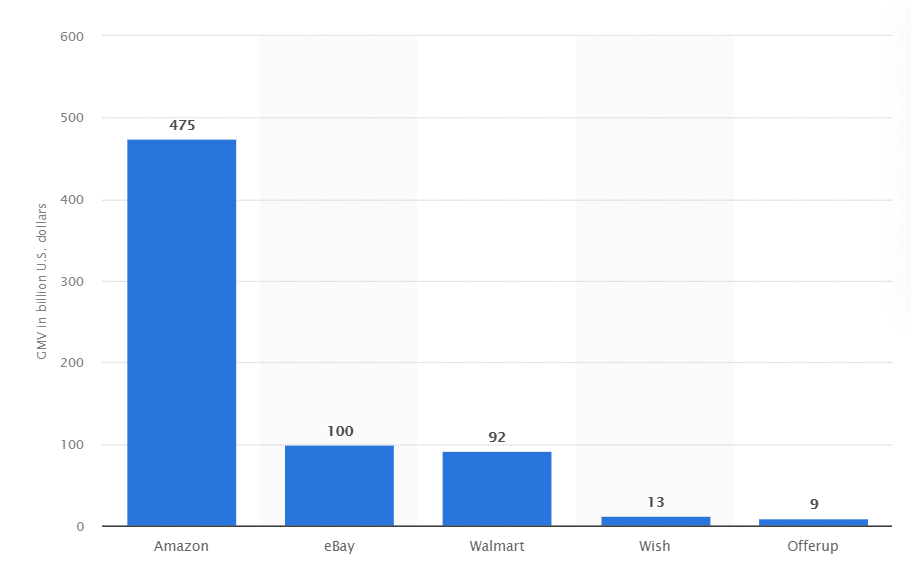

In 2020, Amazon had about $500 billion GMV (Gross Merchandise Value) going through its US E-com site. US total retail was somewhere around $5-6 trillion (depends which data you look at). This means that Amazon already has somewhere around 8-10% of total US retail.

Assuming the nominal value of retail ($5-6 trillion) grows by 4% per year, this means around $200-240 billion of retail sales dollars are up for grabs each year. How much of these can Amazon claim in the US? 30%? 50%?

Let’s say 30%, for example – this would enable Amazon to capture around $60-70 billion additional GMV per year. And how about the offline-to-online retail conversion? Is this trend likely to continue? Or has it somehow reached saturation?

Maybe we’ll end up with an end state of around 35% of all retail converting online in 5 years – up from around 13-15%. This means our initial total US retail pool of $5-6 trillion goes somewhere between $1.75 trillion and $2.1 trillion online, up from $860 billion. How much of this conversion does Amazon capture?

The calculation above means there is around an additional $1 trillion of GMV up for grabs in the next 5 years. Maybe Amazon gets around 50% of this, meaning around $100 bn extra per year.

Combining the share of US retail growth, and online-to-offline conversion, we end up with $160-170 of GMV growth per year for Amazon in this scenario. This means around 30% growth over 2020 GMV. But by the time it gets to 2024 GMV of around $1.1 trillion, the extra $160-170 billion only produces 14% year-over-year.

Adding all this up, if you want to bet on the continued 30% topline growth of the total Amazon company, you’ll have to assume a few things:

The company can find another source of growth to redirect capital into once US E-commerce is saturated (seems easy, given that they have Cloud, International, Logistics, and other businesses growing very fast).

US E-commerce business doesn’t require increasingly huge amounts of capital to defend (Etsy, Pinterest, Instagram, and several others are investing heavily in claiming their part of the E-commerce pie – meaning that customer acquisition costs go up across the board, see my post about this).

The end-state of US E-commerce is not 35% of total retail, but potentially a much higher amount like 50% or 60% - of which Amazon continues to claim a high share.

None of this seems totally unreasonable to me… I’ll be watching carefully to see how this all shakes out.

Game Selection Part 2

I love the idea of “Game Selection” as articulated by fund manager Yen Liow on this podcast. He talks about focusing on unfair fights, where one has an advantage over the rest of the field. I thought this was a brilliant way of looking at the investment game.

Market systems can be brutal. They only attribute value to certain things, and some of these markets have winner-take-all effects. For example, in tennis, almost everyone knows Roger Federer and the market pays him well, but the 1000th best tennis player is barely paying his bills. As such, it makes sense to focus on selecting games in which I have an advantage. If I’m the only person in a small town who can fix iPhones, then I probably have a market advantage that people would pay for.

Yen’s talk, however, brought me back to investing, and which games I should select to play in where I have an actual advantage.

Firstly, as an individual investor, I can probably get into smaller stocks than large players, for whom a 50m market cap stock wouldn’t move the needle, even if it was a great bet. Secondly, I can invest with a longer time horizon, given that all my capital is locked up indefinitely (barring emergencies). I can probably also concentrate into fewer names and tolerate the accompanying volatility better than a standard institutional investor answering to many investors on a weekly or daily basis.

I probably have an unfair advantage in industries in which I have deep knowledge, know the players, and know how the machine works. Some consumer goods companies and tech companies would probably fit into this bucket. Therefore, it probably makes sense to focus on these to start with.

Finally, I can invest in those businesses themselves that are engaged in unfair fights. Oligopolies that can invest heavily behind their competitive advantage while still having enough cash to return to shareholders fit this bill. Or else a tiny software company that has 90% market share of a tiny niche like software for doctors’ practices in Vienna.

It all sounds simple – after all, this is always what we’re searching for in our own lives. I realized this early on when I briefly tried to play rugby in New Zealand, and quickly realized - after seeing that the competition was 30cm taller and twice my width - my best shot at a good life would be instead to focus on getting good grades at school and later getting into business.

Yen explains that game selection requires a bit of honest appraisal about our actual strengths – and the ability to quickly stop any games in which we don’t have some sort of advantage. Charlie Munger talked about Warren Buffett in this interview, saying that Buffett stopped playing golf at age 50 once he realized that he wasn’t getting better. I think an underrated source of Buffett’s success has been very careful game selection.

Baijiu Reflections

I read this interesting article in Bloomberg about Jiangxiaobai, an alcoholic spirits company in China, started in 2012. Inspired by the success of Moutai, and the rapid growth of the Chinese consumer economy, it aims to take share in the huge, growing beverage market of China.

What struck me about this article is a few different brainwaves:

Firstly, as per my post in “Brands Should Invest in Low Self-Esteem Countries”, it seems that Chinese consumers are no longer lusting for Western brands, which symbolized being part of the global economy and being cool. The Chinese people are keener to try local flavors and have the trust in local players to perform in terms of quality and appeal. I believe the trend towards more localized brands will continue in places such as India and China.

Secondly, consumer brands are attracting huge swaths of venture capital from places like Sequoia, which in the US grew their franchise investing primarily in technology companies. Consumer brands have huge growth runways ahead of them in China, and therefore present many potential homeruns for VCs entering the space. This means that many foreign CPG players who thought they had first dibs on the Chinese CPG space are now probably going to earn lower returns on capital, with VC capital also chasing after deals.

Thirdly, what’s interesting to me is that baijiu company Moutai is not going away any time soon. Though Jiangxiaobai can build a baijiu brand and still capture a niche in the market, the premium brand image still belongs to Moutai. Moutai has hundreds of years of branding into the Chinese psyche. Bottles of it can retail anywhere from $300-$4000 depending upon the type and buyer. Understanding Moutai drove home the understanding of the missed opportunity I had with Ferrari. Though other cars exist, Ferrari stands in a league of its own in terms of the status it gives the buyer. I guess the comparison between a Rolex and a Swatch makes a similar point.

Thanks for reading! Remember to share Capital Buddha with friends and colleagues if you think they could benefit from it.